Beyond the Tariff: What Really Shapes a BESS Bid

While many are busy debating the final tariffs in the recent MSEDCL BESS tender, comparing it with the RVUNL bid is like

comparing apples to oranges. Each tender has its own structure, assumptions, and risk contours - and direct comparison

only distorts perspective.

The RVUNL bid was designed for a 2-hour, 2-cycle system with 132kV or 220kV connectivity, where the land and 1.5-2 km

transmission line had to be arranged by the bidder. In contrast, the MSEDCL tender was for a 2-hour, single-cycle-per-day

system with auxiliary consumption, 33kV connectivity and land provided by MSEDCL

- a structure that inherently reduces

capex, simplifies execution, and extends asset life (close to 20 years). Even the auxiliary consumption (which is a major

power drainer) falls under the scope of MSEDCL.

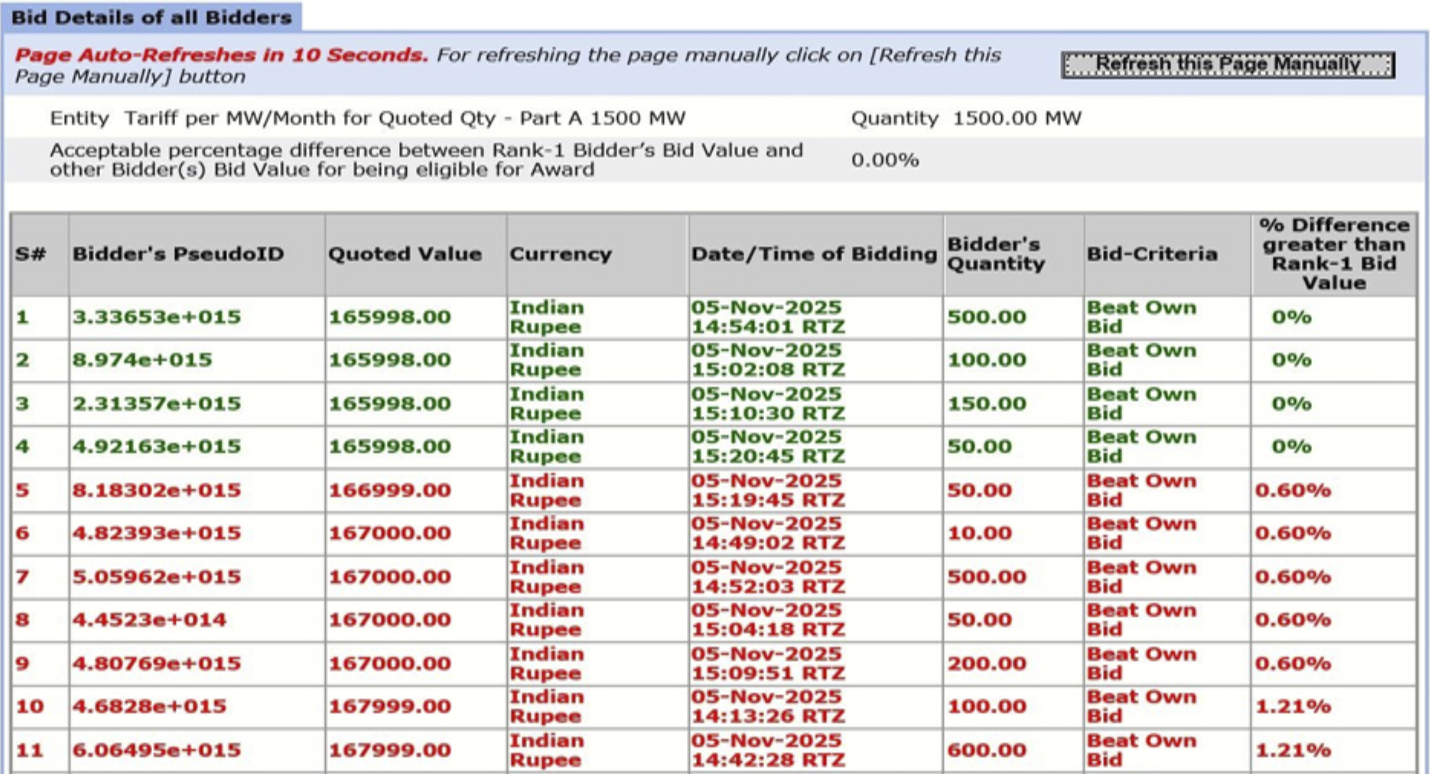

If you look closely, the Z1.65 lakh/MW/month tariff in MSEDCL is actually more attractive than Z1.78 lakh/MW/month in

RVUNL, especially considering the 14%+ IRR in MSEDCL versus single-digit returns in the latter. Our own internal

benchmarks were =1.70 Lakh/MW/Month as the first cut. 71.65 Lakh as the second, and 7162 Lakh as the final threshold

(final "take-it-or-leave-it" threshold).

Too often, we get anchored to historical numbers and lose sight of context. It's like comparing NHPC/SECI ISTS Solar +

BESS projects with RUMSL's 600MW + 440MWh Solar + Storage or UPPCL's standalone BESS (which is effectively Solar + BESS).

Each tender has its own technical architecture, performance obligations, and financial sensitivities and the tariff is merely a

reflection of those underlying realities.

The kev takeaway: Ever bid must be evaluated on its own technical and financial merits. not iust the headline tariff. Otherwise.

we risk losing the forest for the trees.

In energy storage, context isn't optional, it's everything.

December 21, 2019 - BY Admin

December 21, 2019 - BY Admin